What do we support?

Eligible SMEs

- Registered (DTI, SEC or CDA)

- With at least 3 years of profitable operations

- With bank (checking) account

- Must show verifiable benefit to people and community (taxes, permits, employment etc.)

Note: Start-ups may be entertained under exceptional cases (high impact livelihood activity).

Qualified Livelihood Activities

- Manufacturing and production

- Processing (food) activities

- Agri and agri-related projects

- Projects related to health, housing and education

- Projects protecting and promoting the environment (waste recycling, solar and clean energy)

Projects with extra-ordinary social development (high) impact are given interest discount.

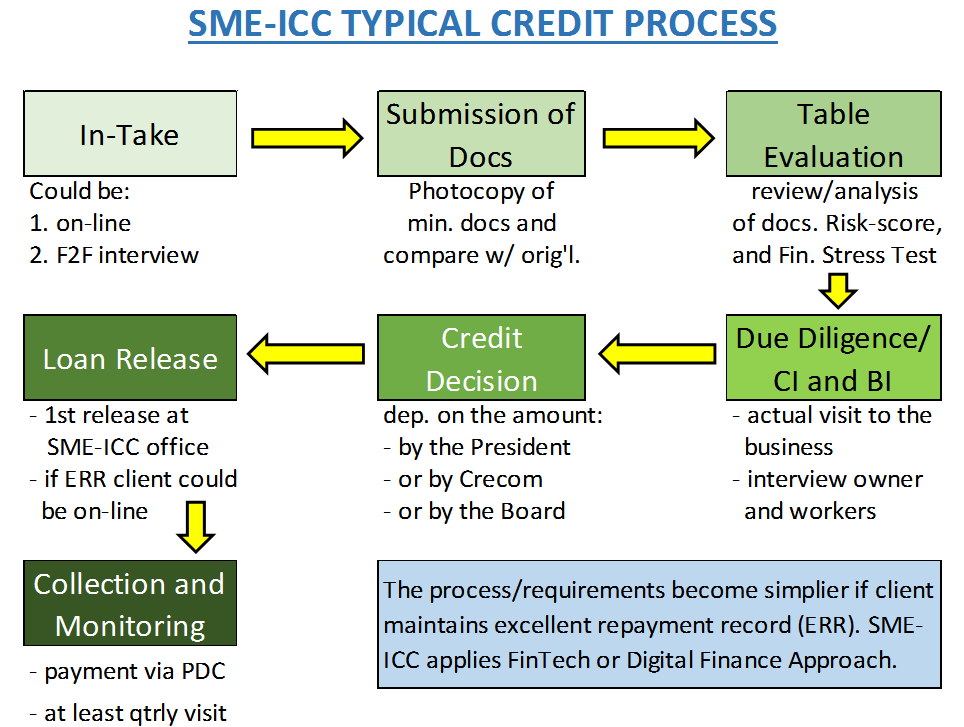

Loan Procedures

- In-Take – quick interview (10-15 mins) to check if SME meets SME-ICC min criteria.

- Submission of Documents – submission of filled-up loan application with attached supporting requirements.

- Table Evaluation – preliminary review of the loan application and documents submitted

- Due Diligence – actual visit to the SME to validate information provided (1 day). Simultaneously, the credit and background investigations are conducted.

- Approval – (or disapproval) within 3 days from submission of complete documents. For re-availing clients with excellent repayment record (ERR Clients), 1-2 days and via FinTech or Digital approval.

- Disbursement/Release – loan is disbursed via check at the SME-ICC office. For ERR clients, loan release is via auto credit to bank account or bank deposit

- Repayment – the SME borrower is required to issue post-dated checks to facilitate collection of loan amortizations.

Documentary Requirements

SME loan applicants should submit:

- Filled-up Loan Application Form (available on-line upon request)

- Photocopy of:

- Business Permit

- DTI – for sole proprietor ( Registration documents )

- SEC – for Corporation and partnership ( Registration documents )

- CDA – for Cooperative ( Registration documents )

- Bank Statements (last 6 months)

- Valid Identification Card

Our Interest Rate

- Higher than bank rate but is significantly lower than other non-bank lenders.

- We are the SMEs’ next best option

- We adopt a risk-based loan pricing (factored in all risks and extend interest discounts for extra-ordinary impact).

Policy on Collateral

Ø We do not approve a loan solely on the basis of collateral neither do we disapprove a loan for reason of lack of collateral.

Ø Collateral is required depending on the amount of loan requested and on the risk profile of the SME borrower.